CIBIL Score for Credit Card – Everything You’d Want to Know

Credit cards are not merely a convenient luxury anymore. They are now a major impact on your financial situation. Your CIBIL Score for Credit Card is the most crucial element in determining your creditworthiness, and credit cards impact it and are impacted by it. If you are seeking your first credit card or wishing to restore a low score, it is essential to know how CIBIL Score for Credit Card and credit cards are related.

In this step-by-step guide, we’ll discuss all you need to know about CIBIL Score for Credit Card approval, how to maintain a good score, and how you can obtain a card even with a poor credit history.

What is a CIBIL Score?

A CIBIL Score for Credit Card ranges from 300 to 900 and is a 3-digit number indicating your creditworthiness. TransUnion CIBIL, one of India’s leading credit bureaus, calculates the score based on your credit history, credit card utilization, loan repayment patterns, defaults, and other financial activities.

Analysis of CIBIL Score Ranges:

| CIBIL Score | Level | Remarks |

|---|---|---|

| 750 – 900 | Excellent | High approval chances with best offers |

| 700 – 749 | Good | Most banks will take applications |

| 650 – 699 | Average | Approval is possible but with lower constraints |

| 600 – 649 | Low | May have to have a secured credit card |

| Under 600 | Poor | High risk for lenders; limited options |

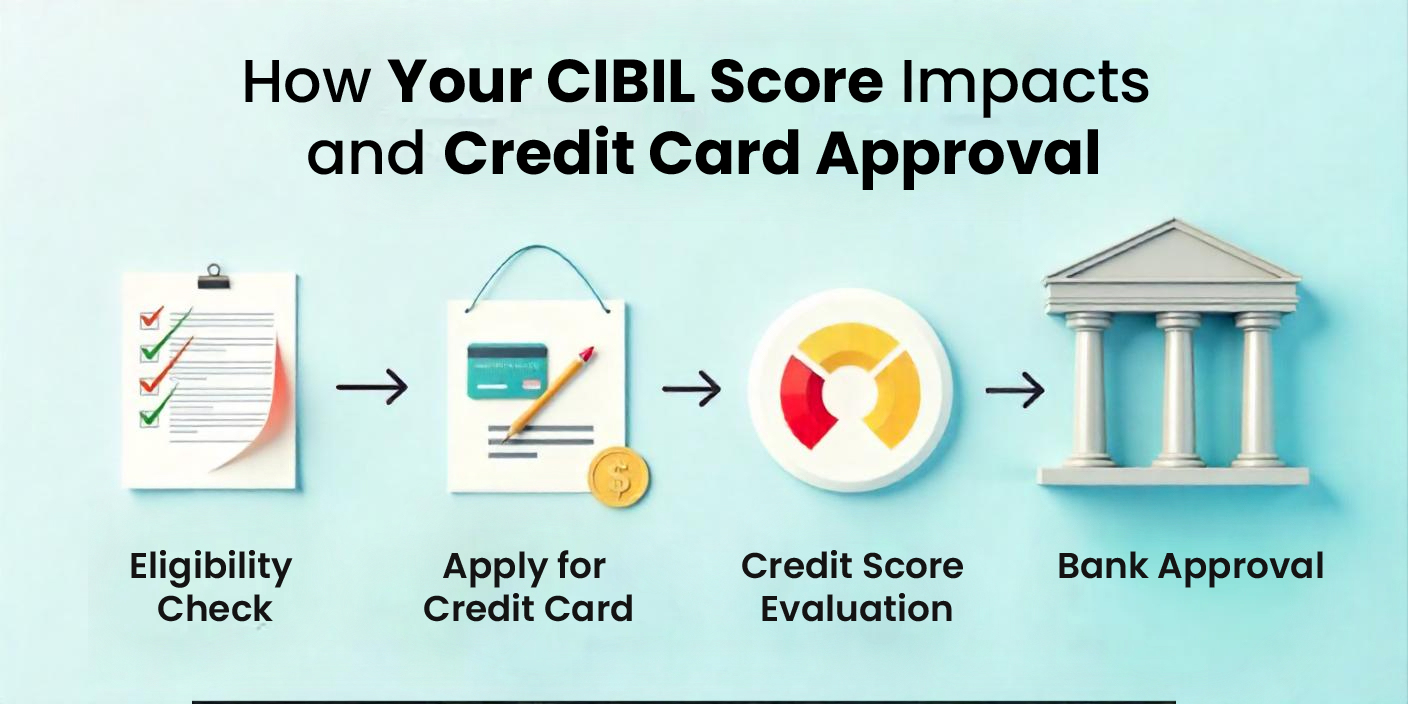

Why Banks Check Your CIBIL Score Before Issuing a Credit Card?

Credit cards are unsecured financial instruments, and therefore there is no collateral supporting them. Banks and NBFCs, therefore, would like to be sure that the candidate is money-wise and can settle dues in a timely manner. The simplest method of doing so is by verifying the candidate’s CIBIL Score for Credit Card.

Here is what banks usually consider:

- Past repayment history

- Number of loans or credit cards held

- Late payments or defaults

- Number of recent credit inquiries

Even no credit history is considered to be risky for some lenders as it informs them of nothing regarding your payment behavior.

Minimum CIBIL Score Required for Credit Card Approval

Generally, a CIBIL Score for Credit Card of 700 and above is preferable to have a regular credit card approved in India. But the figure can be a bit different depending on the bank or the credit card.

CIBIL Score Table:

| CIBIL Score Range | Approval Prospects | Notes |

|---|---|---|

| 750 – 900 | Extremely High | Qualifying for premium cards |

| 700 – 749 | High | Standard cards, good limits |

| 650 – 699 | Medium | May get basic or secured cards |

| Under 650 | Low | Mostly eligible for secured cards only |

How to Get a Credit Card with a Low or No CIBIL Score?

If your CIBIL Score for Credit Card is poor or you do not have a score since you have no credit history, do not fret—there are options.

- Secured Credit Cards

They are credit cards obtained against a fixed deposit (FD). They are less difficult to get because the FD is used as collateral. If paid and utilized within time, they improve your CIBIL Score for Credit Card over a period of time. - Add-on Credit Cards

If a close relative of yours possesses a good-standing credit card, you can ask them to make you an authorized user. This does not establish your own individual credit score, but allows you to gain good usage. - Fintech Cards or NBFCs

A few of the upcoming generation fintech players also provide credit cards to low or no CIBIL Score for Credit Card customers, typically backed by alternative credit rating.

How to Enhance or Maintain Your CIBIL Score?

Maintaining a good CIBIL Score for Credit Card requires vigilant and prudent financial behavior. Some key tips are mentioned below:

- Pay on Time: Pay your credit card payments on or prior to the due date.

- Keep Your Credit Utilization at or Below 30%: Don’t hit your credit limits.

- Limit Hard Inquiries: Too many loan or card inquiries lower your score.

- Monitor Your Credit Report: Look for fraud or mistakes on a regular basis.

- Keep a Credit Mix: A mix of secured (car/home loan) and unsecured (cards) credit helps your score.

- Avoid Closing Old Credit Cards: Older cards contribute to your credit history length.

How to Avoid Credit Card Fraud and Preserve Your Score

Credit card fraud increases, and a single fraudulent transaction can also impact your funds and even your CIBIL Score for Credit Card.

Tips to Stay Safe:

- Update Your Contact Information: Ensure your phone number and email address are up to date to get notifications.

- Don’t Ignore Phishing Calls and Emails: Banks will never ask your card number or OTP.

- Use Only Secure Portals: Make transactions only on websites that start with “https://”.

- Check Statements Frequently: Report the suspicious transaction immediately.

- Report Misuse Immediately: Report to your bank immediately upon loss or misuse.

How to Check Your CIBIL Score?

You can see your credit report and score on the CIBIL website.

How to verify your CIBIL Score for Credit Card:

- Visit the CIBIL website.

- Fill in your own information (name, DOB, PAN, etc.).

- Verify answers by checking your credit history.

- Pay a small amount (around ₹470, although this can fluctuate).

- Download your Credit Information Report (CIR).

Bonus Tip: Some banks and financial websites offer free credit score checks. Utilize them periodically to monitor your CIBIL Score for Credit Card well-being.

Frequent Questions on CIBIL Score for Credit Card

Q1. What is the lowest CIBIL score required for obtaining a credit card?

A minimum of 700 or higher is usually required, but the banks will provide secured credit cards for lower scores.

Q2. Is it possible to obtain a credit card with a 670 CIBIL score?

Maybe, but it might be accompanied by a smaller credit limit and fewer perks.

Q3. Will having more than one credit card increase my CIBIL score?

Not. How responsibly. That’s up to you. High use or delayed payments can damage your score.

Q4. Is it possible to get a credit card with no CIBIL history?

Yes, you can be eligible for secured credit cards or fintech cards by alternative credit data.

Q5. What is the credit limit with a 700 CIBIL score?

The credit limit depends on the issuer and income profile but, with a credit score of 700+, you can be eligible for mid-tier cards.

Q: Does checking my CIBIL score reduce it when applying for a credit card?

A: No, checking your own CIBIL Score for Credit Card eligibility is a soft inquiry and doesn’t impact your score.

Final Thoughts

Your CIBIL Score for Credit Card is more than a number; it’s your economic fingerprint. When you’re applying for a credit card, a good score not only increases chances of approval but also gets you higher rewards, lower interest rates, and improved limits.

Even if you possess a poor credit rating, don’t worry. Start with a secured card, make timely payments, and you will be well on your way to financial independence in no time.

Check Your CIBIL Score for Credit Card Free Now → Click here

Apply for Secured or Beginner-Friendly Credit Cards → Click Here

Vikas Saini: Published on 30/05/2025 12:40:31 PM

Disclaimer

The information, products, and services on this site is for general information purposes only. We try to make sure all content is accurate and update promptly, but sometimes there may be errors, delays, or Mistakes.

The information provided on this site is not a substitute for professional financial, legal, or other advice. Before making financial decisions or using any product/service, we encourage you to read the relevant documents or terms and conditions carefully. If you want guidance regarding your personal situation you should speak to a qualified advisor.If you find any errors, please contact us.

*All services are subject to applicable terms and conditions.